Your Tax Return Is Already Old News

Why last year’s return should become this year’s plan

WEEKLY BLOG 6/1/26 – 6/5/26

Your tax return may be finished.

That does not mean the work is done.

In fact, for planning purposes, the most important part may just be starting.

A tax return tells the story of what already happened. Income earned. Deductions taken. Gains realized. Credits used. Taxes paid. Refund received or balance due.

That is useful.

But it is also old news.

By the time a return is filed, the year it describes is already over. The decisions that created the result were made months ago. Sometimes years ago.

The real opportunity is not just preparing the return correctly. The opportunity is using the return to make better decisions before the next one is written.

The Return Is a Map

Most people see a tax return as a form.

Think of it more like a map.

It shows where income came from: wages, business income, retirement distributions, interest, dividends, capital gains, rental income.

It shows how much flexibility exists. How much was withheld. Whether estimated payments were needed. Whether deductions were meaningful. Whether charitable giving was planned or simply recorded.

It shows whether a household is building wealth efficiently, or just paying taxes after the fact.

That is the part that gets missed when tax work and financial planning are separated. The tax preparer may do a good job filing the return. The advisor may do a good job managing investments. But if those conversations are not connected, the client can still miss the planning opportunity sitting right in front of them.

Source: IRS Publication 505 — Tax Withholding and Estimated Tax; IRS Tax Withholding Estimator

A Refund Is Not Always a Win

This is one of the simplest examples.

A refund feels good. It feels like found money.

But a large refund may also mean too much money was withheld during the year. That may be fine for some people; forced savings is not the worst thing in the world.

But for others, it may mean cash flow was tighter than it needed to be. It may mean money that could have gone toward debt, savings, retirement contributions, or a business opportunity sat with the IRS instead.

A balance due tells a different story.

It may be a one-time issue. Or it may be a sign that income changed, withholding was too low, investment income increased, or estimated payments were not coordinated well enough.

Neither result is automatically good or bad. The question is what it tells us.

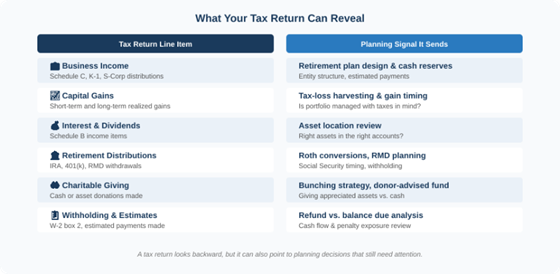

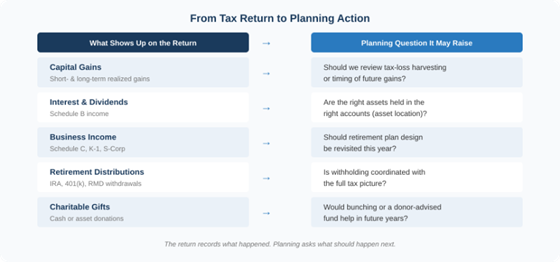

The Hidden Planning Lines

Some of the most important planning opportunities do not jump off the page.

They hide in plain sight.

Capital gains may raise a question about tax-loss harvesting or whether a portfolio is being managed with taxes in mind.

Interest and dividend income may raise a question about asset location.

Business income may raise a question about retirement plan design, entity structure, cash reserves, or estimated payments.

Retirement distributions may raise a question about withholding, Roth conversions, Social Security timing, or future required minimum distributions.

Charitable giving may raise a question about bunching deductions, donor-advised funds, or giving appreciated assets instead of cash.

None of these ideas are automatic recommendations. They are questions. But good planning starts with better questions.

Source: IRS Publication 505 — Tax Withholding and Estimated Tax; IRS 2026 Form 1040-ES; IRS Tax Withholding Estimator

April Is Too Late For Some Decisions

This is the part people learn the hard way.

Many tax-saving moves have to happen before December 31. Some have to happen even earlier.

By the time the return is being prepared, the window has often closed. At that point, the conversation becomes: “Here is what happened.”

Planning changes the conversation to: “Here is what we can still do.”

That is why the middle of the year matters. There is still time to:

- Adjust withholding

- Revisit estimated payments

- Think about capital gains and losses

- Evaluate retirement contributions

- Plan charitable giving

- Review whether income this year looks different from income last year

The tax return gives us the starting point. The plan gives us the next move.

This Is Where Integration Matters

This is also where having tax and planning under one roof can make a real difference.

Not because it creates magic. The rules are still the rules. The market is still uncertain. Tax law is still complicated. Life still changes.

The value is coordination.

When the tax team and planning team are looking at the same facts, the conversation gets better. The tax return is not just filed and archived. It becomes part of the planning process.

That can help identify gaps earlier. It can help avoid surprises. It can help turn tax data into practical decisions about cash flow, investments, retirement, and giving.

That is the goal. Not complexity for the sake of complexity. Better decisions, made earlier.

The Return is Done. The Year Is Not.

There may be more value in your completed tax return than you realize.

It is not just a record of last year.

It is a planning document for this year.

And the earlier we look at it that way, the more useful it becomes.

Disclosure

This is general education and not a substitute for personalized tax, legal, or investment advice. Your situation should be reviewed with the appropriate professionals before taking action. Advisory services offered through NewEdge Advisors, LLC, a registered investment adviser.

Sources

IRS, Publication 505, “Tax Withholding and Estimated Tax.”

IRS, 2026 Form 1040-ES, “Estimated Tax for Individuals.”

IRS, Tax Withholding Estimator.

IRS, Topic No. 306, “Penalty for Underpayment of Estimated Tax.”

| Time (ET) | Report |

| MONDAY, JUNE 1 | |

| 9:45 AM | S&P final U.S. manufacturing PMI |

| 10:00 AM | ISM manufacturing |

| 10:00 AM | Construction spending |

| 11:50 PM |

Minneapolis Fed President Neel Kashkari

speech in South Korea

|

| TBA | Auto sales |

| TUESDAY, JUNE 2 | |

| 8:55 AM |

Cleveland Fed President Beth Hammack

speech

|

| 10:00 AM | Job openings |

| WEDNESDAY, JUNE 3 | |

| 8:15 AM | ADP employment |

| 9:00 AM |

Federal Reserve governor Michael Barr

speech

|

| 9:45 AM | S&P final U.S. services PMI |

| 10:00 AM | Factory orders |

| 10:00 AM | ISM services |

| 2:00 PM | Fed Beige Book |

| THURSDAY, JUNE 4 | |

| 8:30 AM | Initial jobless claims |

| 8:30 AM | U.S. productivity |

| 8:30 AM |

Richmond Fed President Tom Barkin

speech

|

| FRIDAY, JUNE 5 | |

| 8:30 AM | U.S. employment report |

| 8:30 AM | U.S. unemployment rate |

| 8:30 AM | U.S. hourly wages |

| 8:30 AM | Hourly wages year over year |

| 3:00 PM | Consumer credit |

| SATURDAY, JUNE 6 | |

| 12:00 PM |

Federal Reserve governor Michael Barr

speech

|

About Amit: I am a first generation American, the son of a working-class Indian family, and I lived through my parents’ struggle to find their place in this country, to put down roots that would sustain them as well as their children in a new land. As they encouraged me to excel in school and fostered my hobbies and interests, I was keenly aware of the dynamic between them. I understood that there was a difference between where they came from individually and where we were now. They worked hard in their individual capacities, but they weren’t always on the same page about financial issues – and that can make or break a family’s future. I didn’t know it at the time, but this laid the groundwork for my passion towards financial services and helping families succeed.