By Paul Broughton

The S&P 500 continues to make new highs and the economy is reopening at a rapid pace. A great deal of this is likely due to the successful Covid vaccination rollout – everyday we’re getting that much closer to normal. As well, the Fed’s current accommodative monetary policies remain firmly entrenched. And Congress just passed a $1.9 trillion coronavirus relief stimulus package and more is coming. Current investing conditions may be as good as they get. We’re coming out of a sudden and sharp recession and what’s so different about this economic recovery is the amount of fiscal stimulus that’s being applied.

Inflation was vilified in the 1970’s and now there’s not enough of it according to the Fed – and the Fed appears to be determined to allow inflation to run hotter than we’ve seen in a few decades (+2.0% for more than a few months). Besides the current zero interest rate policy, the Fed continues to buy a combined $120 billion per month of Treasuries and mortgage debt, and the Fed’s balance sheet has expanded from about $4.2 trillion pre-pandemic to over $7.7 trillion today – an increase of 83% and growing. The amount of fiscal stimulus to date to fight Covid-19 is just under $6 trillion – this exceeds the total spent fighting World War II (in inflation adjusted dollars, the U.S. spent $4.1 trillion). During the Great Financial Crisis (GFC) a total of $1.8 trillion was spent over five years (about 2.4% of GDP). The nearly $6 trillion that’s being applied to fight Covid-19 is being applied in a much shorter amount of time. Further, the Biden administration is proposing a $2.65 trillion American Jobs Plan and is finalizing an approximately $1.5 trillion American Families Plan. The amounts approved will likely get smaller before being implemented, though. These numbers are obviously significant and that combined fiscal and monetary stimulus is going into an economy that is already forecast to grow at a 6.3% rate this year according to Bloomberg – a level not seen since 4Q 1984.

The Fed’s willingness to allow inflation to run higher seems to be due to a subtle shift in emphasis toward maximizing employment since inflation has been tamed since the late 1990s. They’ve repeatedly said that reducing unemployment for lower-wage workers, who were the most impacted by the pandemic, is one of their most pressing objectives. While the Fed has set a target of 2.0% for inflation, based on the PCE Deflator (U.S. Personal Consumption Expenditure Price Index), it has made clear that it would like to see this rate exceed 2.0% for more than a few months to balance the many years it has run below 2.0%. They haven’t quantified how many – you can only assume that they’ll know when they get there, however long that may be.

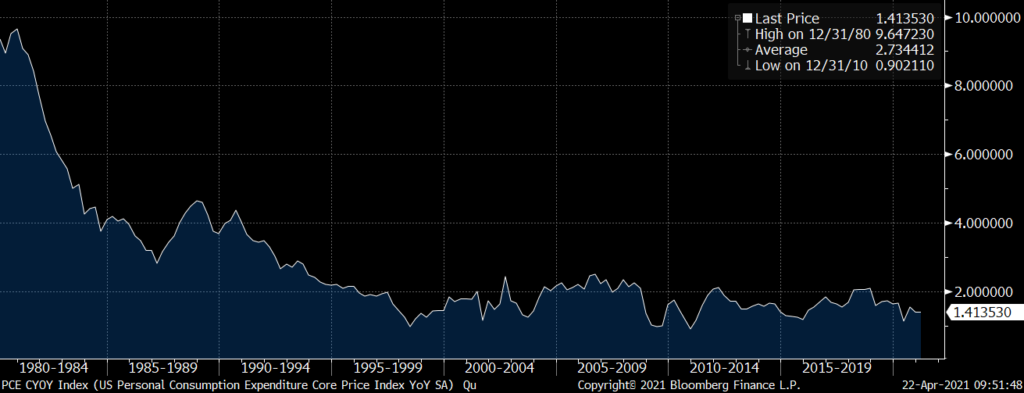

Paul Volcker and Alan Greenspan successfully tamed the great inflation of the 1970’s – it wasn’t easy and you could argue that it took about twenty years to get inflation to 2.0% or lower. Below is a graph of the core PCE since 1980. You can see the steady decline beginning in the early 80’s and then it essentially levels out over the last twenty+ years (it’s averaged 1.7% since 2000).

Current financial conditions are about as healthy as they can possibly get – low interest rates, low inflation, tight credit spreads and a booming economy. All of this is being reflected in equity markets right now. Credit spreads are close to record tight levels due to the extraordinary fiscal and monetary stimulus. Tight spreads are a positive sign for growth prospects: they imply relatively low borrowing costs for businesses. Banks want to lend and the capital markets can raise funds quickly in this current healthy lending environment. As well, consumer balance sheets have greatly improved as credit card usage dropped over the past year and as personal net worth increased along with rising home values, 401k balances, and personal savings. And corporate balance sheets on average are flush with cash.

Also, importantly, the Goldman Sachs Financial Conditions Index* is now at its most accommodative level since its inception in 1982 – this is largely due to the aforementioned tight credit spreads, low Treasury rates, and a weaker U.S. dollar.

All of this is positive for equity investing, but investors need to be mindful that those conditions can change quickly. Inflation has been subdued for more than twenty years and the Fed is intent on allowing it rise enough to significantly reduce unemployment. Moreover, the current environment around credit right now is about as healthy as it can possibly get. When, and if, we do get that lift in inflation, the Fed will start talking about tapering bond purchases, and we’ll see how risk assets respond. Something to keep in mind is that the Fed’s attempts to lift inflation to a level above 2.0% since the Great Financial Crisis haven’t been successful to date. The difference this time might be the very large amounts of fiscal stimulus.

*Goldman Sachs Financial Conditions Index or FCI: A financial conditions index (FCI) summarizes the information about the future state of the economy contained in these current financial variables. Ideally, an FCI should measure financial shocks – exogenous shifts in financial conditions that influence or otherwise predict future economic activity.

ACM is a registered investment advisory firm with the United States Securities and Exchange Commission (SEC). Registration does not imply a certain level of skill or training. All written content on this site is for information purposes only. Opinions expressed herein are solely those of ACM, unless otherwise specifically cited. Material presented is believed to be from reliable sources and no representations are made by our firm as to another parties’ informational accuracy or completeness. All information or ideas provided should be discussed in detail with an advisor, accountant or legal counsel prior to implementation. All investing involves risk, including the potential for loss of principal. There is no guarantee that any investment plan or strategy will be successful. ©ACM Wealth