Freedom Is Built Before You Need It

WEEKLY BLOG 6/29/26 – 7/3/26

This weekend, America turns 250.

There will be fireworks. Flags. Parades. Cookouts. Speeches about freedom.

And all of that matters.

But in real life, freedom usually looks quieter than that.

It looks like choices.

The ability to leave a bad job without blowing up your family’s finances. The ability to help your kids without wrecking your retirement. The ability to care for aging parents without creating a crisis in your own household. The ability to survive a hard year without everything collapsing.

That is not as exciting as fireworks.

But it is a lot more practical.

The National Archives notes that the Continental Congress adopted the Declaration of Independence on July 4, 1776. On July 4, 2026, the country marks 250 years since that moment.

That is a good time to think about what independence actually means in our own lives.

Not as a slogan.

As a plan.

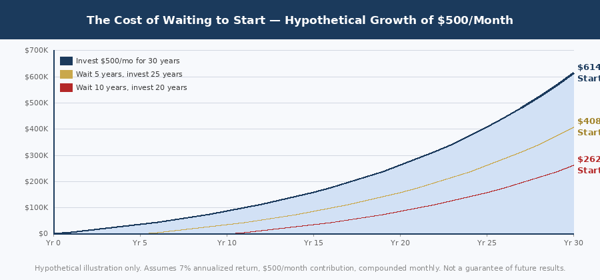

Hypothetical illustration only. Assumes 7% annualized return, $500/month contribution, compounded monthly. Not a guarantee of future results. For educational purposes only.

Freedom Is Not Just Having Money

A lot of people hear “financial independence” and immediately think of a number.

A certain portfolio balance. A certain income level. A certain retirement age.

But money by itself does not create independence.

I have seen people with high incomes who feel trapped. Trapped by spending. Trapped by debt. Trapped by taxes. Trapped by a business they cannot step away from. Trapped by a lifestyle that requires everything to go right.

I have also seen people with more modest resources who feel far more in control because they made intentional decisions over time.

That is the part people miss.

Freedom is not just having money.

Freedom is having structure around the money so it can actually serve you.

Know What You Own

We have talked recently about AI, technology, and the danger of assuming you understand what you own just because a portfolio looks familiar.

That idea applies beyond investments.

Do you know where your money actually goes each month?

Do you know how much risk you are really taking?

Do you know which accounts are taxable, tax-deferred, or tax-free?

Do you know what happens to your plan if markets are down, taxes rise, your income changes, or someone in the family needs help?

Most people do not need more financial products.

They need more clarity.

Because when you do not know what you own, where the risk is, or how the pieces connect, you are not really independent. You are just hoping the system works.

Hope is not a plan.

Do Not Wait for Outside Forces to Save You

We have also talked about the Fed, interest rates, inflation, and the temptation to wait for someone else to make life easier.

Maybe rates will come down.

Maybe inflation will cool.

Maybe markets will broaden out.

Maybe taxes will be lower in the future.

Maybe.

But a good plan should not require one perfect outcome.

That is the whole point.

Independence is built by controlling what you can control before you are forced to. Cash reserves. Debt decisions. Savings rates. Portfolio risk. Tax strategy. Estate documents. Insurance. Beneficiary designations. Retirement timing.

None of those things are exciting.

But they are what give you options later.

And options are what freedom looks like in real life.

Taxes Are Part of the Freedom Equation

This is where planning and tax work have to talk to each other.

Because taxes are not just something you file once a year and forget about. Your tax return is a map. It can show income patterns, missed deductions, concentration risk, business-owner planning gaps, charitable opportunities, Roth conversion windows, capital gains issues, and retirement income problems before they become painful.

That is why the planning side and the tax side cannot live in separate worlds.

A Roth conversion is not just an investment decision. It is a tax-bracket decision.

Charitable giving is not just a generosity decision. It can be a tax-planning decision.

Selling an appreciated investment is not just a portfolio decision. It is a capital-gains decision.

Retirement income is not just about how much you withdraw. It is about where you withdraw from, when you withdraw, and what that does to your tax picture over time.

Because our tax and planning teams sit at the same table, we can look at those decisions together. Not after the fact. Before the move is made.

That is where a lot of value lives.

Not in predicting the market.

In avoiding unforced errors.

Money Is for Choices

At the end of the day, this is what money is actually for.

Not just statements. Not just returns. Not just charts.

Choices.

The choice to slow down. The choice to keep working because you want to, not because you have to. The choice to help family. The choice to be generous. The choice to walk away from something that no longer fits. The choice to absorb a hard season without panic.

That kind of freedom is not built in the moment you need it.

It is built years earlier through small, boring, consistent decisions.

Saving when nobody is watching.

Keeping debt manageable.

Investing through uncomfortable markets.

Planning for taxes before December.

Reviewing documents before there is a crisis.

Having the hard conversations while everyone is healthy.

No magic.

No shortcuts.

Just work done ahead of time.

Final Thought

Two hundred and fifty years later, freedom is still worth thinking about.

Not just as a national idea.

As a personal one.

Because financial independence is not about escaping responsibility. It is about having enough control, clarity, and flexibility to live with more intention.

That does not happen by accident.

It happens when the plan is built before the pressure arrives.

So enjoy the fireworks this weekend.

But when the noise quiets down, ask a better question.

What would more freedom actually look like in your life?

And are you planning for it now, or hoping it shows up later?

Sources

National Archives — Declaration of Independence

America250 — America’s 250th Anniversary

|

Time (ET)

|

Report |

| Monday, Jun. 29 | |

| No events scheduled | |

| Tuesday, Jun. 30 | |

| 9:00 AM | S&P Cotality Case-Shiller Home Px Index |

| 9:45 AM | Chicago Business Barometer – ISM-Chicago Business Survey – Chicago PMI |

| 10:00 AM | Conference Bd – Consumer Confidence |

| 10:00 AM | Job Openings & Labor Turnover Survey |

| Wednesday, Jul. 1 | |

| 8:15 AM | ADP National Employment Report |

| 9:45 AM | US Manufacturing PMI |

| 10:00 AM | ISM Report On Business Manufacturing PMI |

| 10:00 AM | Construction Spending |

| Thursday, Jul. 2 | |

| 8:30 AM | Weekly Jobless Claims |

| 8:30 AM | Employment Report |

| 8:30 AM | Unemployment Rate |

| 8:30 AM | Avg Hourly Earnings, M/M% |

| 8:30 AM | Avg Hourly Earnings, Y/Y% |

| 10:00 AM | Factory Orders |

| Friday, Jul. 3 | |

| No events scheduled |

About Amit: I am a first generation American, the son of a working-class Indian family, and I lived through my parents’ struggle to find their place in this country, to put down roots that would sustain them as well as their children in a new land. As they encouraged me to excel in school and fostered my hobbies and interests, I was keenly aware of the dynamic between them. I understood that there was a difference between where they came from individually and where we were now. They worked hard in their individual capacities, but they weren’t always on the same page about financial issues – and that can make or break a family’s future. I didn’t know it at the time, but this laid the groundwork for my passion towards financial services and helping families succeed.

IMPORTANT NOTICE AND DISCLOSURE

The information and material contained in this communication is confidential and intended for the recipient addressee named. If you are not the intended recipient please delete the message and notify the sender immediately.

NewEdge Advisors, LLC is an Investment Adviser registered with the Securities and Exchange Commission. Any information provided has been obtained from sources considered reliable, but we do not guarantee the accuracy or the completeness of any description of securities, markets or developmentsmentioned. As a precautionary measure, we cannot rely on e-mail requests to authorize, direct or effect the purchase or sale of any security, wire transfer, or to affect any other transactions. Such requests, orders, or other instructions sent by email should be confirmed verbally, prior to their anticipated execution. We are unable to ensure email sent to you from us, or sent from you to us will be received. Please contact us at 845-652-3449 if there is any change in your financial situation, needs, goals or objectives, or if you wish to initiate any restrictions on the management of the account or modify existing restrictions. Additionally, we recommend you compare any account reports from NewEdge Advisors LLC with the account statements from your Custodian. Please notify us if you do not receive statements from your Custodian on at least a quarterly basis. Our current disclosure brochure, Form ADV Part 2, is available for your review upon request. This disclosure brochure, or a summary of material changes made, is also provided to our clients on an annual basis. This material was prepared with the assistance of AI. All content has been reviewed, edited, and approved by Forefront Wealth Planning prior to use. This is general education and not a substitute for personalized tax, legal, or investment advice. Your situation should be reviewed with the appropriate professionals before taking action. Advisory services offered through NewEdge Advisors, LLC, a registered investment adviser.