Inflation Isn’t Gone. It Just Changed Shape.

Why Prices Still Feel High Even When Inflation “Falls”

Weekly Blog Post — May 17–23, 2026

The market wants to believe inflation is yesterday’s problem. Consumers and small businesses are telling a different story. The risk now is not a repeat of 2022 exactly. It is a stickier, more uneven inflation cycle that keeps pressure on households, complicates the Fed’s job, and makes financial planning more important than market guessing.

Inflation has a funny way of disappearing from the headlines before it disappears from real life.

For a while, the market narrative was fairly straightforward: inflation had cooled, the Federal Reserve was closer to cutting rates, and the economy had managed to avoid the recession many people had been expecting. Stocks liked that story. Investors liked that story. Frankly, everyone wanted to like that story.

But the last few weeks have been a reminder that inflation does not always move in a straight line. It does not simply show up, go away, and stay gone.

Sometimes it rotates.

It moves from used cars to insurance. From goods to services. From wages to energy. From headline prices to the costs businesses absorb before consumers ever see them.

And that is where we are now.

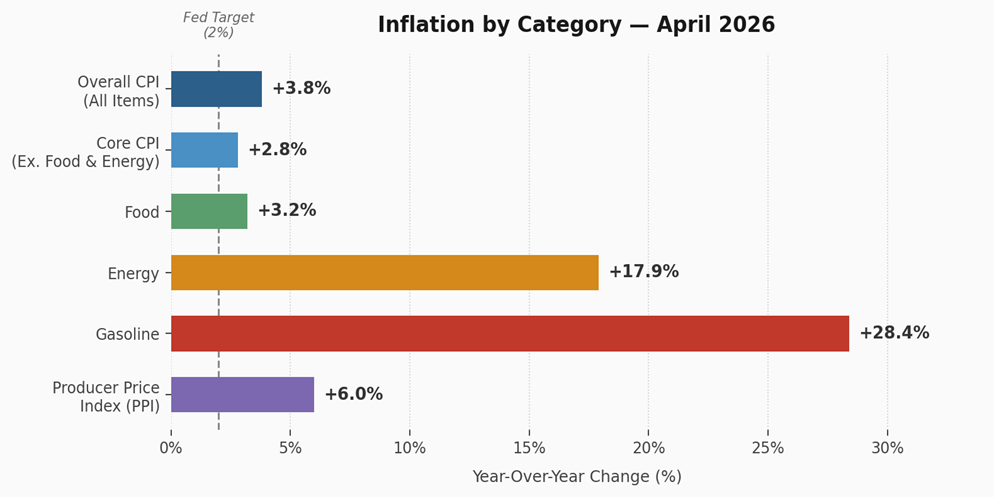

The April Consumer Price Index showed prices up 3.8% from a year ago. Energy prices were up 17.9%, gasoline was up 28.4%, and food was up 3.2%. Core inflation, which excludes food and energy, was lower at 2.8%, but still above the Federal Reserve’s long-term 2% target.

At the same time, producer prices rose sharply in April. The Producer Price Index increased 1.4% for the month and 6.0% from a year earlier. That matters because producer prices often represent pressure building underneath the surface. They are the costs businesses face before deciding whether to absorb them, pass them along, cut expenses elsewhere, or accept lower margins.

That is the part of the inflation story worth paying attention to.

Not because we should panic. Not because 2022 is necessarily repeating itself. But because the market may be a little too eager to declare the inflation problem solved.

Inflation is not one thing

One of the mistakes people make is talking about inflation as if it is a single number.

It is not.

There is consumer inflation, which is what households feel when they buy groceries, fill the car, pay insurance premiums, book travel, or renew a lease.

There is producer inflation, which is what businesses feel when input costs rise.

There is wage inflation, which is good for workers but can become challenging for businesses if productivity does not keep up.

There is asset inflation, which can make portfolios look better while making homes, education, and retirement more expensive.

And then there is lifestyle inflation, which is not caused by the economy at all, but by our own tendency to let spending rise as income rises.

For many high-earning households, especially HENRYs — high earners not rich yet — inflation is not always felt as an inability to pay the bills. It is felt as a slower path to wealth.

The family can still take the vacation, but it costs more. The mortgage payment is still manageable, but the property taxes, insurance, utilities, and maintenance feel heavier. The income is still strong, but the amount left over for investing, college planning, charitable giving, or future flexibility is smaller than expected.

For retirees and those close to retirement, the issue is different but just as important. Inflation challenges the confidence behind the plan. A portfolio may be well-built, but rising living costs can make withdrawals feel more uncomfortable. Healthcare, housing, insurance, travel, and family support all become more meaningful when the paycheck is no longer replenishing the account every two weeks.

This is why inflation is so personal. The official data matters, but no one lives inside an economic average.

The Fed’s problem just got harder

The Federal Reserve has been trying to bring inflation back toward 2% without causing unnecessary damage to the economy.

That is easier said than done.

At its April meeting, the Fed left its target rate range unchanged at 3.50% to 3.75%. The statement also noted that inflation was elevated, in part because of higher global energy prices, and that developments in the Middle East were contributing to uncertainty in the economic outlook.

That is a difficult setup.

If inflation keeps cooling, the Fed has more flexibility to cut rates. Lower rates can help borrowers, businesses, homebuyers, and markets.

But if inflation reaccelerates, especially because of energy or supply-chain pressure, the Fed has less room to ease. Cutting rates too soon could risk adding fuel to the fire. Holding rates too high for too long could create stress in housing, credit, small businesses, and parts of the economy that are already sensitive to financing costs.

That is the balancing act.

Markets tend to focus on what the Fed might do next. But households and businesses live with what rates already are.

For a family trying to buy a home, refinance debt, fund college, or balance savings goals, the difference between a lower-rate world and a higher-rate world is not theoretical. It changes cash flow.

For business owners, higher borrowing costs affect inventory, hiring, equipment purchases, and expansion plans.

For retirees, rates are more complicated. Higher yields can improve income opportunities in cash and bonds, but inflation can still erode purchasing power if the overall plan is not designed thoughtfully.

This is why the Fed matters, but it should not become the center of your financial plan. A good plan should not depend on one perfect interest-rate path.

Why this feels worse than the data

I have had more than one conversation recently where someone has said some version of the same thing: “I keep hearing inflation is improving, but my monthly spending does not feel any better.”

That is the disconnect.

One reason inflation is so frustrating is that people often hear “inflation is coming down” and think that means prices are coming down.

That is not what it means.

When inflation slows, prices are generally still rising — just at a slower pace. The higher price level remains.

That is why a 3% or 4% inflation rate can still feel uncomfortable after several years of elevated price increases. People are not comparing today’s grocery bill, insurance premium, or vacation cost to last month. They are comparing it to what life used to cost.

And that gap is real.

The University of Michigan’s latest consumer sentiment survey showed that sentiment remained under pressure in May, with current economic conditions falling from April and consumers citing high prices as a major concern for both personal finances and major purchases. Year-ahead inflation expectations also remained elevated at 4.5%.

That lines up with what many people feel.

The stock market may be near highs. The economy may still be expanding. Unemployment may be relatively stable. But if your monthly burn rate is higher, your insurance premiums are up, travel costs more, and your long-term goals require more capital than they used to, it is understandable that the economy feels better on paper than it does in real life.

This is especially true for high earners in expensive areas like New Jersey, New York, and the broader tri-state region. A strong income does not automatically create financial freedom when housing, taxes, childcare, college planning, elder care, and lifestyle costs are all competing for the same dollars.

And for retirees, the feeling can be even more emotional. Inflation does not just raise expenses. It can raise the fear of outliving assets, even when the plan is still fundamentally sound.

That is why we should not dismiss the way people feel just because the data looks manageable.

Sometimes the data is accurate, and the feeling is accurate too. They are just measuring different things.

What investors should do

The first thing investors should do is avoid turning every inflation report into an investment strategy.

Reacting month to month is rarely helpful.

Inflation data is noisy. Markets are forward-looking. The Fed is data-dependent. Geopolitical events can change the energy picture quickly. And investors who constantly shift portfolios based on the latest headline often end up creating more risk than they remove.

That said, inflation should not be ignored.

It should be planned for.

For working households, that means knowing your true savings rate after lifestyle costs. It means being honest about whether income growth is building wealth or simply funding a more expensive version of the same life. It means keeping enough liquidity so that higher costs do not force bad decisions.

For retirees and near-retirees, it means stress-testing the plan. What happens if living costs rise faster than expected for a few years? What happens if healthcare expenses increase? What happens if markets are volatile at the same time withdrawals are needed? These are not predictions. They are planning questions.

For business owners, it means watching margins, not just revenue. Sales can look healthy while profitability quietly erodes. Inflation often shows up in the business before it shows up in the household.

For investors, it means maintaining a portfolio that does not require one perfect outcome. Stocks, bonds, cash, and alternative sources of return each have different roles. Cash provides flexibility. Bonds can provide income and stability. Equities help fight long-term inflation. Diversification is not exciting, but it exists for environments exactly like this one.

The goal is not to predict every inflation print.

The goal is to build a financial life that can absorb uncertainty without forcing emotional decisions.

Inflation may not be the crisis it was a few years ago. But it is also not gone. It has changed shape.

And when the shape of risk changes, the answer is not to panic.

The answer is to pay attention, revisit assumptions, and make sure the plan still fits the world we are actually living in — not the one the market wants to believe in.

Sources

U.S. Bureau of Labor Statistics, Consumer Price Index Summary — April 2026. CPI, energy, gasoline, food, and core inflation figures. Bureau of Labor Statistics

U.S. Bureau of Labor Statistics, Producer Price Index News Release — April 2026. PPI monthly and year-over-year figures. Bureau of Labor Statistics

Federal Reserve, FOMC Statement — April 29, 2026. Federal funds target range, 2% inflation objective, elevated inflation and Middle East uncertainty. Federal Reserve

University of Michigan, Surveys of Consumers — Preliminary May 2026 Results. Consumer sentiment, current economic conditions, price concerns, and year-ahead inflation expectations. sca.isr.umich.edu

| Time (ET) | Report |

| MONDAY, MAY 18 | |

| 8:30 AM |

Atlanta Fed First Vice President Cheryl

Venable welcoming remarks

|

| 10:00 AM | Home builder confidence |

| TUESDAY, MAY 19 | |

| 8:00 AM | Fed governor Christopher Waller speech |

| 10:00 AM | Pending home sales |

| 7:00 PM |

Philadelphia Fed President Anna Paulson

speech

|

| 7:45 PM |

Atlanta Fed First Vice President Cheryl

Venable closing remarks

|

| WEDNESDAY, MAY 20 | |

| 9:15 AM | Fed governor Michael Barr speech |

| 2:00 PM | Minutes of Fed’s May FOMC meeting |

| THURSDAY, MAY 21 | |

| 8:30 AM | Initial jobless claims |

| 8:30 AM | Housing starts |

| 8:30 AM | Building permits |

| 8:30 AM | Philadelphia Fed manufacturing survey |

| 9:45 AM | S&P flash U.S. services PMI |

| 9:45 AM | S&P flash U.S. manufacturing PMI |

| 12:20 PM |

Richmond Fed President Tom Barkin

speech

|

| FRIDAY, MAY 22 | |

| 10:00 AM | Consumer sentiment (final) |

| 10:00 AM | U.S. leading economic indicators |

| 10:00 AM | Fed governor Christopher Waller speech |

About Amit: I am a first generation American, the son of a working-class Indian family, and I lived through my parents’ struggle to find their place in this country, to put down roots that would sustain them as well as their children in a new land. As they encouraged me to excel in school and fostered my hobbies and interests, I was keenly aware of the dynamic between them. I understood that there was a difference between where they came from individually and where we were now. They worked hard in their individual capacities, but they weren’t always on the same page about financial issues – and that can make or break a family’s future. I didn’t know it at the time, but this laid the groundwork for my passion towards financial services and helping families succeed.