We Still Haven’t Found What We’re Looking For

The economy is doing fine on paper. GDP grew around 2 percent in Q1. The stock market keeps pushing to new highs.

But that’s not how it feels.

Consumers feel tight. Small businesses feel cautious. And that gap between what the data say and what people experience keeps widening.

That disconnect matters.

We came into 2026 expecting a strong, broad recovery. What we got instead is something more fragile. Growth is happening, but it’s concentrated. The economy is holding up, not breaking out.

Call it a “good enough” economy. It’s being held together by massive tech investment, and consumers are spending more while saving less.

That’s not the same thing as strength.

The Economy We Were Promised

At the start of the year, the setup looked good.

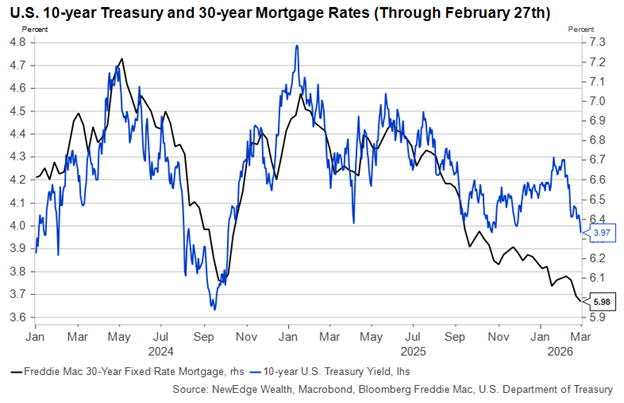

Tax cuts hadn’t fully kicked in yet. Tariff pressure was fading. Rates were falling. Mortgage rates dipped below 6 percent. That should have helped housing and construction wake up.

Expectations followed that story.

We had two concerns at the time.

The labor market appeared to be losing momentum. And stock prices were already assuming everything would go right.

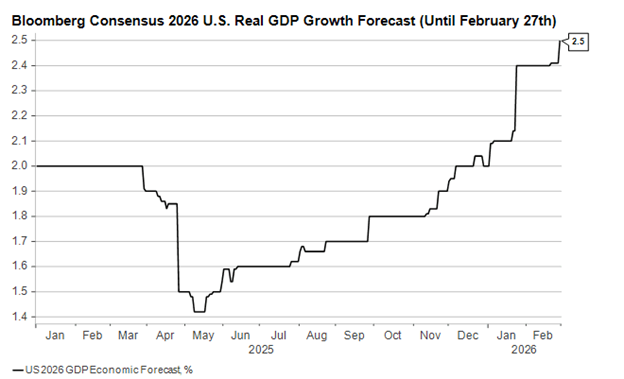

Still, falling rates gave us some optimism.

As of 2/27/26

Then Q1 GDP came in solid.

As of Q1 2026

Some of that strength was timing related, especially around government shutdown effects. But even after stripping that out, private sector demand improved.

So far, so good.

But the surface numbers don’t tell the full story.

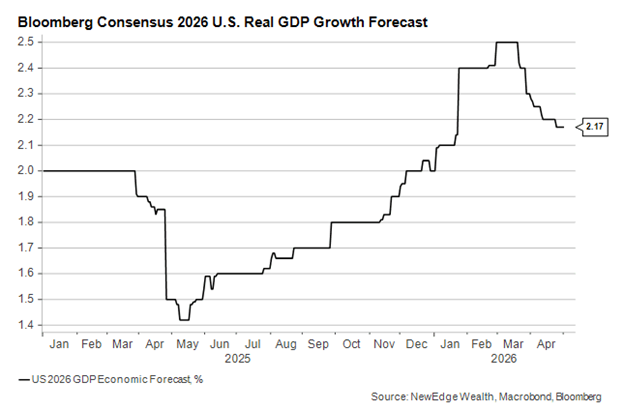

We’re Not Going Back to February

The environment changed quickly.

The conflict in Iran pushed oil prices higher. Interest rates followed. Gas above $4.25 and a 10-year Treasury near 4.5 percent is not what the economy needed.

You can see expectations start to roll over.

As of 5/1/26

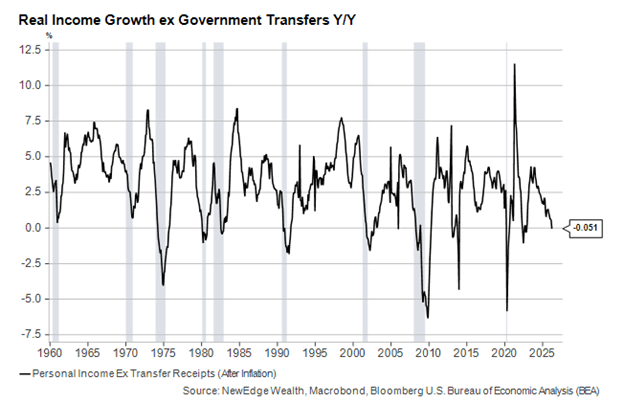

This hits consumers first.

Real income growth was already slow. Inflation pushed it negative over the past year. That doesn’t happen often outside of tougher economic periods.

As of March 2026

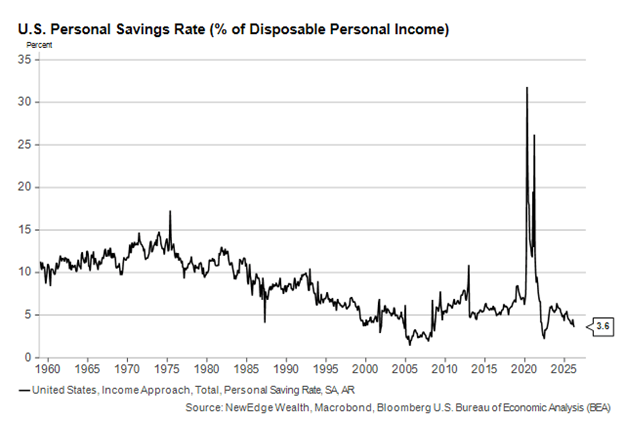

Yet spending hasn’t collapsed.

Why?

Because people are saving less.

The savings rate has dropped to 3.6 percent. That’s a meaningful decline.

As of March 2026

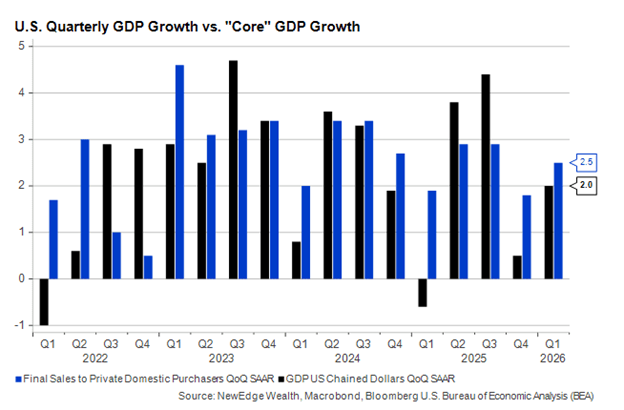

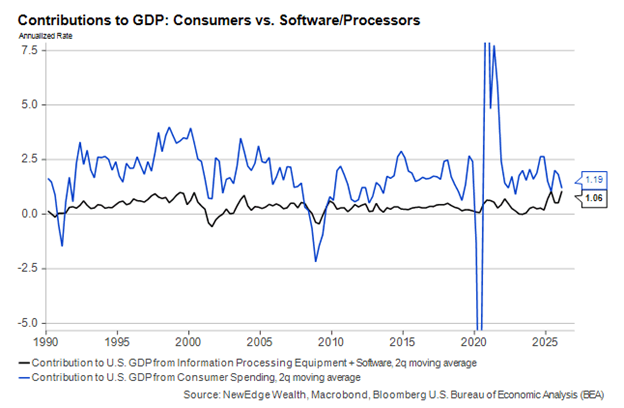

At the same time, growth is being driven by a very specific place.

Technology investment. AI. Chips. Infrastructure around computing.

That’s carrying a big part of the load.

As of Q1 2026

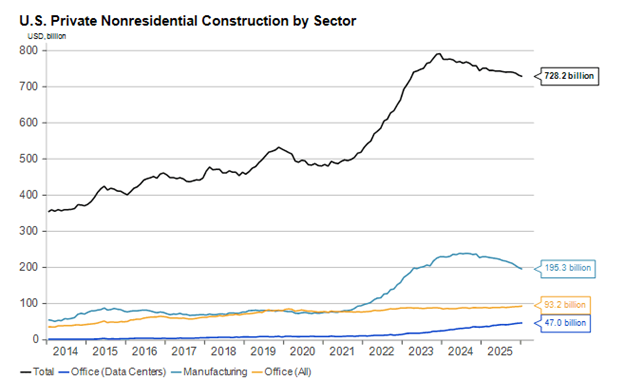

Outside of that, things look weaker.

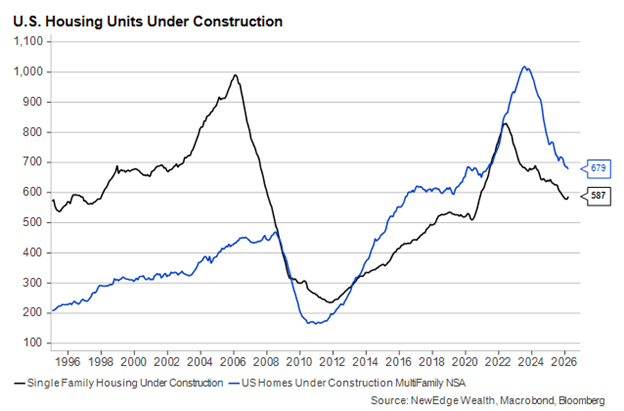

Commercial construction outside of data centers is down. Housing has declined for five straight quarters. The broader construction boom never showed up.

Even with a recent small bounce, housing activity is still well below where it used to be.

As of March 2026

So, here’s the reality.

We have strong growth in a few areas. Pressure on consumers. And parts of the economy that feel closer to a slowdown than an expansion.

That’s not what most people expected coming into the year.

The Labor Market Is Holding Up

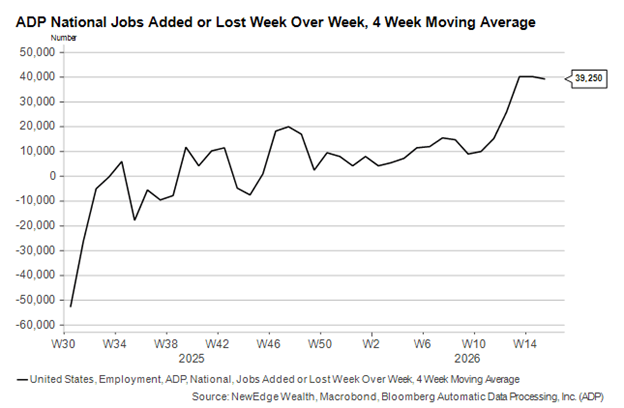

If there’s a stabilizer right now, it’s jobs.

Hiring has improved.

As of 4/30/2026

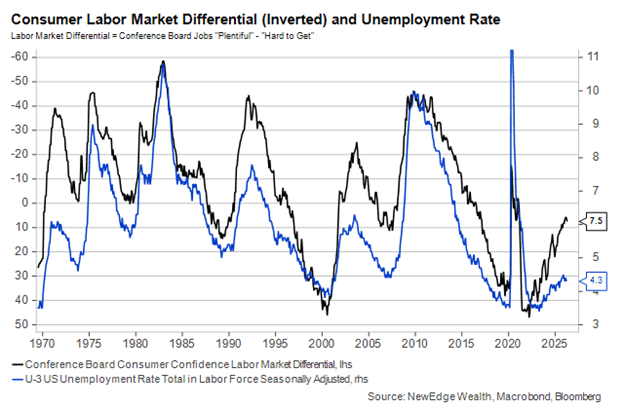

Jobless claims are near historic lows. People feel a bit better about job availability.

As of April 2026

That matters.

A weakening labor market would have forced the Fed’s hand. Instead, they have room to stay patient.

That reduces one of the bigger risks we were watching.

Conclusion: Narrow Growth Leads to Narrow Markets

Earnings have held up. In some cases, they’ve improved faster than stock prices, which has kept valuations from getting stretched again.

But there’s a catch.

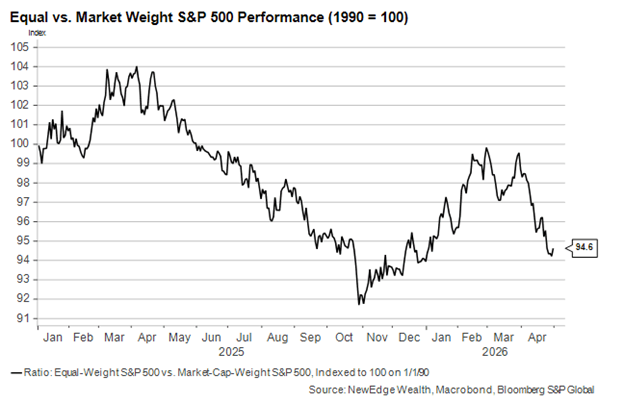

That earnings growth is concentrated. A small group of companies, mostly tied to AI, are doing the heavy lifting.

The market is reflecting that.

As of 4/30/26

When leadership narrows, the biggest companies tend to pull further ahead. That’s exactly what we’re seeing.

So, the economy and the market are telling the same story.

Growth is happening, but it’s not broad.

From here, two things matter.

First, can growth expand beyond tech and AI?

Second, can the consumer keep spending without the support of rising incomes?

Right now, there’s not much evidence that growth is about to broaden. At the same time, there’s also no clear sign that the AI-driven investment cycle is slowing down.

That leaves us in the middle.

Not weak. Not strong. Just concentrated.

And that’s why things still don’t feel quite right.

| Time (ET) | Report |

| MONDAY, MAY 4 | |

| 10:00 AM | Factory orders |

| 12:50 PM | New York Fed President John Williams speech |

| TUESDAY, MAY 5 | |

| 8:30 AM | U.S. trade balance |

| 10:00 AM | Job openings |

| 10:00 AM | New home sales* (delayed report) |

| 10:00 AM | New home sales |

| 9:45 AM | S&P final U.S. services PMI |

| 10:00 AM | ISM services |

| 10:00 AM | Fed Vice Chair for Supervision Michelle Bowman |

| speech | |

| 12:30 PM | Fed Governor Michael Barr speech |

| WEDNESDAY, MAY 6 | |

| 8:15 AM | ADP employment |

| 9:30 AM | St. Lous Fed President Alberto Musalem speech |

| 1:00 PM | Chicago Fed President Austan Goolsbee speech |

| THURSDAY, MAY 7 | |

| 8:30 AM | Initial jobless claims |

| 8:30 AM | U.S. productivity |

| 10:00 AM | Construction spending* (delayed report) |

| 10:00 AM | Construction spending |

| 1:00 PM | Minneapolis Fed President Neel Kashkari speech |

| 2:05 PM | Cleveland Fed President Beth Hammack speech |

| 3:00 PM | Consumer credit |

| 3:30 PM | New York Fed President John Williams speech |

| FRIDAY, MAY 8 | |

| 5:45 AM | Fed Governor Lisa Cook speech in Senegal |

| 8:30 AM | U.S. employment report |

| 8:30 AM | U.S. unemployment rate |

| 8:30 AM | U.S. hourly wages |

| 8:30 AM | Hourly wages year over year |

| 10:00 AM | Wholesale inventories |

| 10:00 AM | Consumer sentiment (prelim) |

| 7:30 PM | Chicago Fed President Austan Goolsbee, San |

| Francisco Fed President Mary Daly, Fed governor | |

| Michelle Bowman, Fed governor Christopher Waller | |

| on a panel |

About Amit: I am a first generation American, the son of a working-class Indian family, and I lived through my parents’ struggle to find their place in this country, to put down roots that would sustain them as well as their children in a new land. As they encouraged me to excel in school and fostered my hobbies and interests, I was keenly aware of the dynamic between them. I understood that there was a difference between where they came from individually and where we were now. They worked hard in their individual capacities, but they weren’t always on the same page about financial issues – and that can make or break a family’s future. I didn’t know it at the time, but this laid the groundwork for my passion towards financial services and helping families succeed.