The Fed Is Waiting. Your Financial Life Shouldn’t.

Why rate decisions matter, but should not run your plan

WEEKLY BLOG 6/1/26 – 6/5/26

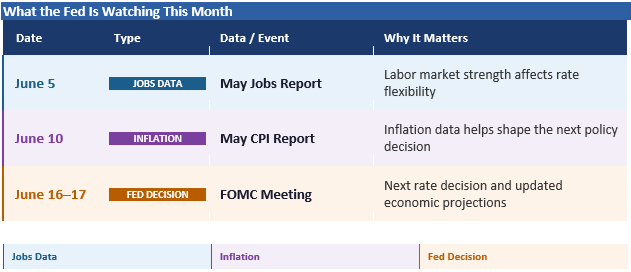

The next two weeks are going to be very Fed-heavy.

The May jobs report just came out. CPI is scheduled for Wednesday. The Fed meets the following week. Markets will spend the next several days debating whether the next move is a cut, a hold, or something else entirely.

That conversation matters.

But it should not become your entire financial plan.

Because while investors are focused on what the Fed might do next, households and business owners are still living with what rates already are.

That is the part that gets missed.

The Fed Is Still in Wait-and-See Mode

In May, the economy added 172,000 jobs and the unemployment rate held at 4.3%. That is not a collapsing labor market. It is also not an overheated one. It is somewhere in the middle, which is exactly what makes the Fed’s job harder.

The Fed’s most recent statement kept the federal funds target range at 3.50% to 3.75%. The message was basically this: inflation is still above target, employment still matters, and the committee wants more data before doing anything dramatic.

That is not exciting.

But it is important.

Markets love certainty. The Fed is not giving them much of it right now.

The Fed’s June Setup

Source: U.S. Bureau of Labor Statistics release calendar; Federal Reserve FOMC calendar.

Rates Show Up Everywhere

Interest rates are not just a Wall Street topic.

They show up in real life.

They affect mortgage rates. Credit cards. Auto loans. Home equity lines. Business lines of credit. Cash yields. Bond income. The cost of refinancing. The value of holding too much cash or too little cash.

For retirees, higher rates can make cash and bonds look more attractive. But they can also create more taxable interest income.

For business owners, higher borrowing costs can make inventory, equipment, hiring, or expansion decisions more difficult.

For young families, rates can change the math on buying a home, upgrading a home, or carrying debt longer than expected.

For high earners, higher cash yields may feel great until the tax bill shows up.

That last part is worth repeating.

A higher yield is not the same thing as a higher after-tax return.

The Tax Angle Most People Miss

This is where the tax conversation and the planning conversation need to be in the same room.

If you are earning more interest in a money market fund, CD, Treasury, or high-yield savings account, that income may be taxable. If your portfolio is generating more dividends or bond income, that may affect your estimated tax payments. If you live in a high-tax state, the type of income matters too.

The investment decision and the tax result are connected.

That does not mean one product or strategy is automatically better. It means the question should be asked before the surprise shows up.

- Where should cash sit?

- Should bonds be held in taxable accounts or retirement accounts?

- Does municipal bond exposure make sense?

- Is your withholding still accurate?

- Do estimated payments need to change?

None of these are Fed predictions. They are planning questions.

Do Not Wait for the Perfect Rate Environment

A lot of people are waiting.

- Waiting for mortgage rates to fall.

- Waiting for the Fed to cut.

- Waiting for inflation to cool.

- Waiting for the market to get easier.

The problem is that waiting can feel responsible while still becoming its own kind of risk.

Cash can sit too long. Debt can compound. Tax bills can build. Portfolios can drift. Business decisions can get delayed past the point where they are still useful.

A good plan does not require one perfect Fed outcome.

It should work across several outcomes.

Maybe rates come down. Maybe they stay higher for longer. Maybe inflation gives the Fed room. Maybe it does not.

The goal is not to guess the next press conference.

The goal is to know what you will do either way.

The Plan Matters More Than the Prediction

The Fed is important.

But the Fed does not know your mortgage, your tax return, your business cash flow, your retirement date, your charitable goals, your college expenses, or your risk tolerance.

That is your plan’s job.

When tax and planning are coordinated, these decisions get better. Not because anyone can predict rates perfectly. No one can. But because the right people are looking at the same facts before decisions get made.

That is the work.

Not guessing the Fed.

Building a financial life that does not depend on guessing the Fed.

Sources

U.S. Bureau of Labor Statistics, Employment Situation Summary, May 2026. https://www.bls.gov/news.release/empsit.nr0.htm

U.S. Bureau of Labor Statistics, 2026 Release Calendar. https://www.bls.gov/schedule/2026/home.htm

Federal Reserve, FOMC Statement, April 29, 2026. https://www.federalreserve.gov/newsevents/pressreleases/monetary20260429a.htm

Federal Reserve, FOMC Meeting Calendar. https://www.federalreserve.gov/monetarypolicy/fomccalendars.htm

| Time (ET) | Report |

| MONDAY, JUNE 8 | |

| None scheduled | |

| TUESDAY, JUNE 9 | |

| 6:00 AM | NFIB optimism index |

| 8:30 AM | U.S. trade balance |

| 10:00 AM | Existing home sales |

| 10:00 AM | Wholesale inventories |

| WEDNESDAY, JUNE 10 | |

| 8:30 AM | Consumer price index |

| 8:30 AM | CPI year over year |

| 8:30 AM | Core CPI |

| 8:30 AM | Core CPI year over year |

| 2:00 PM | Monthly U.S. federal budget |

| THURSDAY, JUNE 11 | |

| 8:30 AM | Initial jobless claims |

| 8:30 AM | Producer price index |

| 8:30 AM | Core PPI |

| 8:30 AM | PPI year over year |

| 8:30 AM | Core PPI year over year |

| FRIDAY, JUNE 12 | |

| 10:00 AM | Consumer sentiment (prelim) |

About Amit: I am a first generation American, the son of a working-class Indian family, and I lived through my parents’ struggle to find their place in this country, to put down roots that would sustain them as well as their children in a new land. As they encouraged me to excel in school and fostered my hobbies and interests, I was keenly aware of the dynamic between them. I understood that there was a difference between where they came from individually and where we were now. They worked hard in their individual capacities, but they weren’t always on the same page about financial issues – and that can make or break a family’s future. I didn’t know it at the time, but this laid the groundwork for my passion towards financial services and helping families succeed.

IMPORTANT NOTICE AND DISCLOSURE

The information and material contained in this communication is confidential and intended for the recipient addressee named. If you are not the intended recipient please delete the message and notify the sender immediately.

NewEdge Advisors, LLC is an Investment Adviser registered with the Securities and Exchange Commission. Any information provided has been obtained from sources considered reliable, but we do not guarantee the accuracy or the completeness of any description of securities, markets or developmentsmentioned. As a precautionary measure, we cannot rely on e-mail requests to authorize, direct or effect the purchase or sale of any security, wire transfer, or to affect any other transactions. Such requests, orders, or other instructions sent by email should be confirmed verbally, prior to their anticipated execution. We are unable to ensure email sent to you from us, or sent from you to us will be received. Please contact us at 845-652-3449 if there is any change in your financial situation, needs, goals or objectives, or if you wish to initiate any restrictions on the management of the account or modify existing restrictions. Additionally, we recommend you compare any account reports from NewEdge Advisors LLC with the account statements from your Custodian. Please notify us if you do not receive statements from your Custodian on at least a quarterly basis. Our current disclosure brochure, Form ADV Part 2, is available for your review upon request. This disclosure brochure, or a summary of material changes made, is also provided to our clients on an annual basis. This material was prepared with the assistance of AI. All content has been reviewed, edited, and approved by Forefront Wealth Planning prior to use. This is general education and not a substitute for personalized tax, legal, or investment advice. Your situation should be reviewed with the appropriate professionals before taking action. Advisory services offered through NewEdge Advisors, LLC, a registered investment adviser.