The Mid-Year Financial Checkup Nobody Actually Does

Why July Is One of the Most Important Months for Your Financial Plan

WEEKLY BLOG 7/13/26 – 7/17/26

Most people think financial planning happens in December.

That is when retirement contributions get topped off, charitable donations are made, and everyone starts asking the same question: “Is there anything I can still do before year-end?”

The honest answer is often, “Maybe.”

By December, many of the best planning opportunities have already passed.

That is why I actually like July better.

We are halfway through the year. There is enough information to know how the year is shaping up, but there is still plenty of time to make meaningful adjustments. Whether you are working toward retirement, saving for college, running a business, or simply trying to be more intentional with your money, now is an ideal time for a financial checkup.

Here are eight things worth reviewing before summer slips away.

1. Check Your Tax Withholding

Life changes faster than tax withholding.

Maybe you received a raise. Changed jobs. Got married. Started consulting on the side. Sold investments. Or had a child.

Any of those can change what you ultimately owe when you file your return.

A quick review now may help reduce the chance of an unpleasant surprise next April. It may also help avoid giving the IRS an interest-free loan if too much is being withheld.

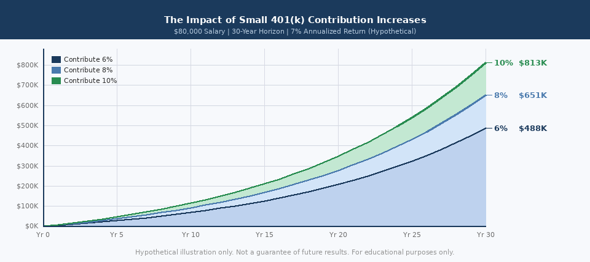

2. See If You’re On Pace With Your 401(k)

Many people choose a contribution percentage in January and never look at it again.

Take a few minutes to see whether your savings are keeping pace with your goals. If you received a raise this year, consider increasing your contribution before lifestyle expenses quietly absorb the extra income.

Even a one or two percent increase can make a meaningful difference over time because of compounding.

If your employer offers a match, make sure you are contributing enough to receive the full benefit. That is one of the few opportunities in investing where the return is immediate.

Hypothetical illustration only. Assumes $80,000 salary, 7% annualized return, compounded monthly. Not a guarantee of future results. For educational purposes only.

3. Review Your HSA Contributions

If you are eligible for a Health Savings Account, it remains one of the most tax-efficient accounts available.

Contributions may reduce taxable income, investments can grow tax deferred, and qualified withdrawals for medical expenses are tax free.

Many people think of an HSA as a checking account for healthcare expenses. In reality, it can also become an important long-term planning tool.

4. Review Your Investment Accounts

The middle of the year is a good time to review your portfolio without reacting to headlines.

Ask yourself a few simple questions.

Are your investments still aligned with your goals?

Has one position become much larger than intended?

Are there opportunities to harvest tax losses or manage capital gains before year-end?

Good investing is often less about making dramatic changes and more about making thoughtful adjustments over time.

5. Review Your Beneficiaries

This is one of the simplest financial tasks and one of the most overlooked.

Beneficiary designations on retirement accounts and life insurance policies generally override instructions in a will.

If you have experienced a marriage, divorce, birth of a child, death in the family, or any other significant life event, make sure your beneficiary designations still reflect your wishes.

This review takes only a few minutes but can prevent major complications later.

6. Update Estate Documents After Major Life Changes

Estate planning is not something you do once and forget forever.

If your family situation has changed, or if it has been several years since your documents were reviewed, this is a good time to revisit your will, powers of attorney, healthcare directives, and any trust documents.

An outdated estate plan can create unnecessary confusion for the people you care about most.

7. Compare Your Spending to Your Goals

The first half of the year usually tells an honest story.

Have your spending habits moved you closer to your goals or farther away?

Summer often brings vacations, camps, weddings, home projects, and other expenses that can quietly stretch a budget. There is nothing wrong with spending on experiences that matter. The key is making those decisions intentionally rather than wondering where the money went in October.

A mid-year review gives you time to make adjustments before the calendar gets crowded again.

8. Estimate Your Year-End Tax Picture

This is one of the biggest reasons July matters.

Rather than waiting until tax season, estimate where you are likely to finish the year.

Will you be in a different tax bracket?

Are there opportunities for Roth conversions?

Should you accelerate deductions or charitable giving?

Would realizing gains or losses this year improve your long-term tax picture?

These are planning conversations, not filing conversations.

The earlier they happen, the more options you usually have.

Planning Works Best Before Deadlines Arrive

One of the biggest misconceptions about taxes is that planning happens when you file your return.

Filing reports what already happened.

Planning influences what happens next.

Many financial decisions carry tax consequences, and many tax decisions affect the broader financial picture. Looking at both sides together — ideally well before year-end — is where a lot of planning value is created.

The goal is not simply to pay less in taxes this year. It is to make better financial decisions over many years.

If you have not looked at your financial picture since January, now is a great time to do it.

Your future self will probably appreciate that you did.

Sources

Internal Revenue Service. Tax Withholding Estimator.

Internal Revenue Service. Retirement Topics: 401(k) and Profit-Sharing Plan Contribution Limits.

Internal Revenue Service. Health Savings Accounts (HSAs).

Internal Revenue Service. Frequently Asked Questions on Gift Taxes, Capital Gains, and Basis.

U.S. Securities and Exchange Commission. Updated Investor Bulletin: Diversification.

Consumer Financial Protection Bureau. Choosing and Updating Beneficiaries.

American Bar Association. Estate Planning Resources.

|

Time(ET)

|

Report |

| Monday, Jul. 13 | |

| 5:25 AM |

Federal Reserve Vice Chair Michelle

Bowman speaks at Bank Policy Institute(BPI)

roundtable

|

| 12:30 PM |

Federal Reserve Governor Governor

Christopher Waller speaks at New York

Association for Business Economics event

|

| 2:00 PM | Monthly Treasury Balance |

| 5:00 PM |

ECB President Christine Lagarde meets

Federal Reserve Chair Kevin Warsh

|

| Tuesday, Jul. 14 | |

| 6:00 AM | NFIB Index of Small Business Optimism |

| 8:30 AM | CPI |

| 8:30 AM | CPI, Y/Y% |

| 8:30 AM | CPI Core, Y/Y% |

| 10:00 AM |

Federal Reserve Board Chair Kevin Warsh

presents Monetary Policy Report to U.S.

House Financial Services Committee

|

| 1:00 PM |

Federal Reserve Bank of Chicago President

Austan Goolsbee speaks at Kenosha Area

Business Alliance Business Lunch

|

| Wednesday, Jul. 15 | |

| 8:30 AM | Empire State Manufacturing Survey |

| 8:30 AM | PPI |

| 8:30 AM | Ex-Food & Energy PPI, M/M% |

| 8:30 AM | Personal Consumption |

| 8:45 AM |

Federal Reserve Bank of New York President

John Williams speaks at Partnership for New

York City event

|

| 10:00 AM |

Federal Reserve Board Chair Kevin Warsh

presents Monetary Policy Report to U.S.

Senate Banking Committee

|

| 1:00 PM |

Federal Reserve Governor Governor Lisa

Cook speaks at Exchequer Club Luncheon

|

| 2:00 PM | U.S. Federal Reserve Beige Book |

| Thursday, Jul. 16 | |

| 8:30 AM | Retail Sales |

| 8:30 AM | Philadelphia Fed Business Outlook Survey |

| 8:30 AM | Weekly Jobless Claims |

| 10:00 AM | Manufacturing & Trade: Inventories & Sales |

| 10:00 AM | NAHB Housing Market Index |

| 10:00 AM | Pending Home Sales Idx, M/M% |

| 12:30 PM |

FRB Dallas President Lorie Logan speaks in

Houston

|

| 7:00 PM |

Federal Reserve Governor Governor Philip

Jefferson speaks at Stanford Institute for

Economic Policy Research event

|

| Friday, Jul. 17 | |

| 8:30 AM | Housing Starts |

| 8:30 AM | Import Prices |

| 9:15 AM | Industrial Production, M/M% |

| 9:15 AM | Capacity Utilization % |

| 10:00 AM | U. Michigan Prelim Consumer Survey |

About Amit: I am a first generation American, the son of a working-class Indian family, and I lived through my parents’ struggle to find their place in this country, to put down roots that would sustain them as well as their children in a new land. As they encouraged me to excel in school and fostered my hobbies and interests, I was keenly aware of the dynamic between them. I understood that there was a difference between where they came from individually and where we were now. They worked hard in their individual capacities, but they weren’t always on the same page about financial issues – and that can make or break a family’s future. I didn’t know it at the time, but this laid the groundwork for my passion towards financial services and helping families succeed.

IMPORTANT NOTICE AND DISCLOSURE

The information and material contained in this communication is confidential and intended for the recipient addressee named. If you are not the intended recipient please delete the message and notify the sender immediately.

NewEdge Advisors, LLC is an Investment Adviser registered with the Securities and Exchange Commission. Any information provided has been obtained from sources considered reliable, but we do not guarantee the accuracy or the completeness of any description of securities, markets or developmentsmentioned. As a precautionary measure, we cannot rely on e-mail requests to authorize, direct or effect the purchase or sale of any security, wire transfer, or to affect any other transactions. Such requests, orders, or other instructions sent by email should be confirmed verbally, prior to their anticipated execution. We are unable to ensure email sent to you from us, or sent from you to us will be received. Please contact us at 845-652-3449 if there is any change in your financial situation, needs, goals or objectives, or if you wish to initiate any restrictions on the management of the account or modify existing restrictions. Additionally, we recommend you compare any account reports from NewEdge Advisors LLC with the account statements from your Custodian. Please notify us if you do not receive statements from your Custodian on at least a quarterly basis. Our current disclosure brochure, Form ADV Part 2, is available for your review upon request. This disclosure brochure, or a summary of material changes made, is also provided to our clients on an annual basis. This material was prepared with the assistance of AI. All content has been reviewed, edited, and approved by Forefront Wealth Planning prior to use. This is general education and not a substitute for personalized tax, legal, or investment advice. Your situation should be reviewed with the appropriate professionals before taking action. Advisory services offered through NewEdge Advisors, LLC, a registered investment adviser.