by Paul Broughton

This past week the S&P 500 made a new all-time high and Apple reached $2 trillion in valuation. It would seem that the pandemic is already in the rearview mirror. After the shortest bear market in U.S. history, a brief 33 days compared to the median of 302 days for the prior twenty bear markets, we also saw the fastest market recovery in history. This makes some sense since this was a public health crisis rather than a fundamentally economic one. However, many worry that Wall Street is disconnected from Main Street, as tens of millions of Americans remain unemployed. As many as 32% of American households owe money for missed rent or mortgage payments, thousands of small businesses are struggling to survive under restricted operations. Is the market’s rise sustainable?

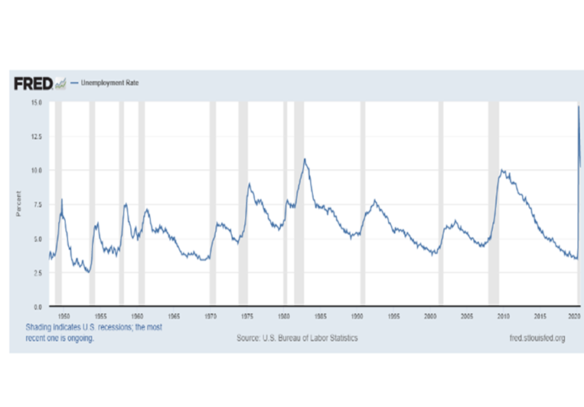

While the market reaches new highs, there are plenty of data showing that the economy continues to struggle in its fight with Covid-19. A good place to start is the absolute level of unemployment at 10.2%. The 14.7% reading in April was the highest level since the Great Depression. Hopefully, this will drop into single digits as we approach year end.

In the most recent Fed minutes released on August 19th, officials said that “the ongoing public health crisis would weigh heavily on economic activity, employment, and inflation in the near term and was posing considerable risks to the economic outlook over the medium term.” Also, the Fed minutes revealed consensus among participants that more fiscal help was needed. Note also that the 10-year Treasury’s current yield of 0.64% says a lot about market participants’ expectations for economic growth over the next ten years. Mortgage delinquincies stand at 8.22% and will likely rise further (see graph below). During the Great Financial Crisis, these didn’t peak until the first-quarter of 2010. Residential foreclosures are currently at record lows due to moratoriums on notices, but, at some point, the moratoriums will be lifted. And commercial real-estate delinquencies for the retail and lodging sectors are close to 15% and 25%, respectively.

As we enter the fall and winter, outdoor dining will be curtailed and people may not be ready to eat inside. Many leisure activities will remain closed or severely limited. Many sporting and entertainment events are cancelled or operating in very limited fashion, with adverse consequences for local businesses that cater to the crowds at these events. Schools are struggling to open, with many engaged in remote learning, impairing the ability of the parents to go back to work.

There are many more points that can be made about how bad things look at the moment. But the market is a forward-looking mechanism and, essentially, it’s saying that our economy is recovering and a vaccine is likely in the offing over the next few quarters – life will return to normalcy soon enough.

Even before a vaccine is available, there are plenty of signs of a solid recovery. The aforementioned low level of interest rates has boosted the housing market. The 30-year mortgage rate is close to 3.00%. The National Association of Home Builders Index, a diffusion index of homebuilder optimism, is near record levels as demand continues to strengthen. Lumber prices are soaring due to the demand. And the iShares U.S. Home Construction ETF is up over 27% year to date compared to the S&P’s 5% rise. We expect the demand for single family homes with a yard and in a good school district to further strengthen as people move from cities to the suburbs.

Industrial activity is also resuming. Consumer spending for services fell sharply during the shut-down, but demand for goods fell only modestly. Since many factories closed temporarily, goods were taken from inventories, which are now quite depleted. So, manufacturing activity is picking up sharply to meet demand and replenish stocks. Household income was supplemented very sharply by assorted government programs and household saving surged from around 9% in Q1 to more than 25% in Q2. Consumers wisely paid down debt, but they now have considerable capacity to also finance spending.

A full recovery will require a vaccine, so activity can return to normal. But a meaningful recovery is already underway, with Q3 data likely to show a rebound in excess of 20% at an annual rate. The equity market is surely anticipating more, perhaps because the effort to develop a vaccine is well funded and widespread along multiple paths. And policy around the world, from central banks to governments, are synchronized in their support. The economic path may be uneven, but the equity market’s optimism may be realized.

ACM is a registered investment advisory firm with the United States Securities and Exchange Commission (SEC). Registration does not imply a certain level of skill or training. All written content on this site is for information purposes only. Opinions expressed herein are solely those of ACM, unless otherwise specifically cited. Material presented is believed to be from reliable sources and no representations are made by our firm as to another parties’ informational accuracy or completeness. All information or ideas provided should be discussed in detail with an advisor, accountant or legal counsel prior to implementation. All investing involves risk, including the potential for loss of principal. There is no guarantee that any investment plan or strategy will be successful. ©ACM Wealth