by Kevin Kelly

Portfolio Manager

Many investors do not realize they are playing with fire in the fixed income portion of their portfolios by choosing to own common, high quality investment grade bonds. The typical, easy to construct investment grade portfolio of brand name bonds will leave investors with low yielding assets that have significant interest rate risk exposure. These investors are likely to be disappointed and could lose money in the next year or two.

The typical basket of investment grade bonds with an average 5-year maturity provides an overall yield of 1% or less. If 5-year interest rates rise by approximately 0.27%, your total return will net out to 0%, as the price decline offsets the initial yield. If interest rates go up more, you will lose money on a full year basis. To help put such an interest rates move in context, the 5-year Treasury is currently only 0.42% and was 1.69% at the end of 2019. We are not forecasting a dramatic interest rate spike, but the upside risk to rates is clearly higher than the downside especially following the recent vaccine news. A 1% yielding portfolio simply provides little room for interest rates to rise.

There are better options. A significantly more attractive fixed income portfolio can be carefully constructed, although that requires meticulous security selection. It is possible to more than double the yield, however, while lowering your interest rate risk. You will have to take a small amount of additional credit risk, but the additional yield is compelling in Advisors Capital Management’s (ACM) opinion. (Reminder: yield = interest rate + credit spread).

The urgency to adjust a traditional fixed portfolio has never been greater. Since I suggested two months ago that investors should reassess their non-ACM fixed income portfolios, the news of two highly effective COVID-19 vaccines has strongly impacted the fixed income market. The vaccine news improved market sentiment, which drove down credit spreads. Improved sentiment lessens the fear component that typically depresses rates. The vaccine news also improves economic growth prospects in 2021, which is putting upward pressure on medium and long-term rates. Therefore, long-term interest rates risk seems more skewed to the upside, but a sizable interest rate decline seems unlikely. When you choose to own A-rated or even higher quality bonds, the credit spread component of yield is small and provides little protection should interest rates rise. As a reminder, credit spreads tighten when the economy is improving.

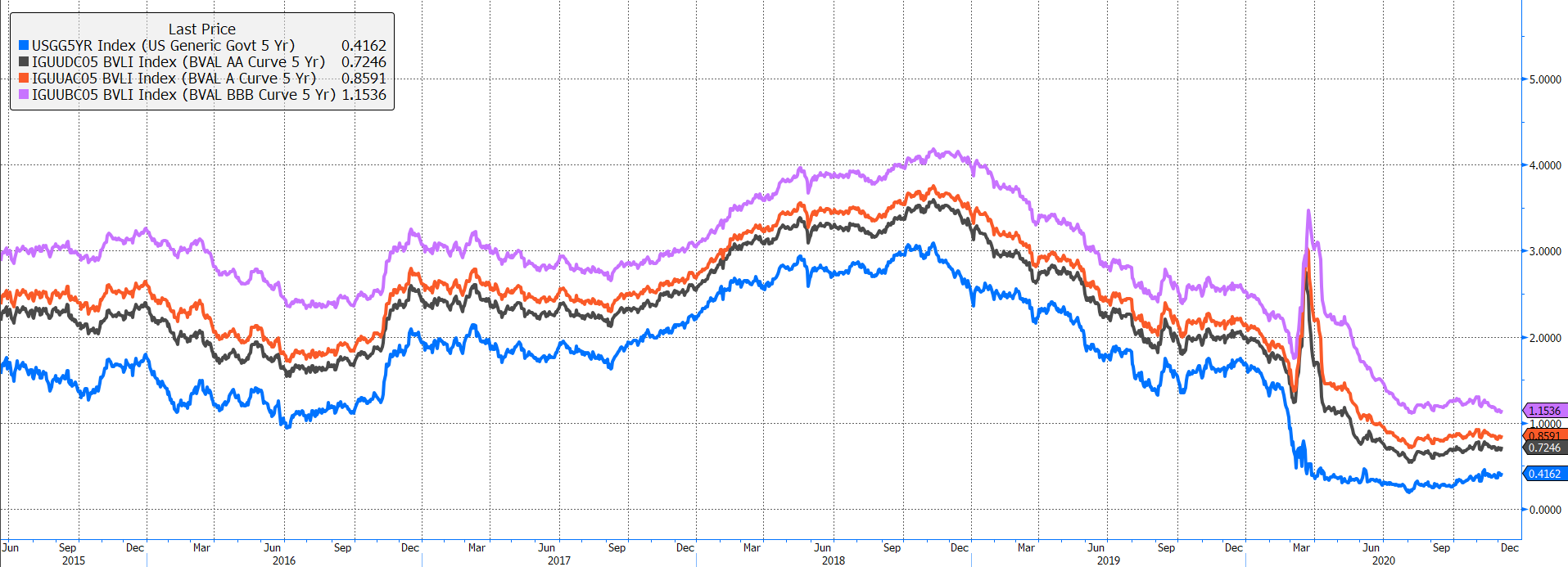

Given the roller-coaster ride of 2020, some investors do not realize how significantly yields have declined in the investment grade market. The table and graph below show more than 50+% yield declines across a range of 5-Year investment grade bonds.

Source: Bloomberg. LLC. Note: Please note we quote benchmark yields which are a based on a large basket of bonds and not necessarily indicative of the yield of our strategies.

I would bet that a survey of a hundred randomly selected investors would show them to be dramatically overestimating their yields on fixed income. Most of their fixed portfolios are yielding below 1% gross (before taxes and inflation). If you only own short-dated bonds of very well-known companies, then your bond portfolio likely yields less than 0.75%. If you want to be extremely ‘safe,’ which is certainly your prerogative, recognize that the cost of safety may be a negative return over the near year, because you are taking considerable interest rate risk. There are three things investors need to remember so they do not grossly overestimate their potential fixed income returns.

3 Important reminders for analyzing your fixed income portfolio

Bond prices have limited upside potential, because as bond prices rise, yields decline.

While stock prices can double or triple, bond prices are capped since they must return to $100 (par value) at maturity. Some investors assume their bond prices can keep going up. Unfortunately, no matter at what price the bond is trading (or price you paid), the company is only going to give you back $100 at maturity, the amount it originally borrowed. This is crucial, since almost all investment grade bonds are currently trading above par. This misperception causes many investors to think they are earning, and can continue to earn, dramatically more than is mathematically possible.

Do not just look at your account balance to see if you are making money in fixed.

If your account statements include both fixed income and equity positions, the statement will not be sufficient to understand the performance and yield of your fixed income positions. For example, in November 2020, the stock market rose over 10% for 2020, while most fixed benchmarks increased only slightly. Your statement may report a solid gain of 7-9%, so you assumed everything was going great, but the gains came from the stock side, not the bonds side. If you own primarily brand name bonds with relatively short maturities, you have little upside, a low yield, and plenty of downside risk. Keep a copy of your November statement handy, so you can monitor your bond prices, which we expect to decline over the next 6-12 months. Even if interest rates do not rise, you will see your bond prices decline towards par as maturity approaches.

Investors often confuse coupons and yield (See Appendix for a detailed explanation).

In a low interest rate environment, coupons dramatically overstate the yield you are earning. Since almost all investment grade bonds are trading above par, the coupons may overstate your yield by as much as 2 to 4 times. Since most currently outstanding investment grade bonds were issued when yields and interest rates were much higher than today, their prices have risen, and their yields have fallen tremendously. Over 30% of investment grade bonds trade at a price over $120 and over 60% of bonds trade above $110. This leads clients to massively overestimate yields when they use coupons as an approximation.

If you own an investment grade portfolio, ask ACM or your advisor to reassess your fixed portfolio. Ask for your yield to maturity for each bond you own, which will reveal the return you will earn holding your bonds to maturity.

The potential cost of not acting to improve your fixed portfolio is substantial. The first four days of December are a great reminder of the potential interest rate risk inherent in a typical, investment grade portfolio. The average A-rated bond lost 0.62% following a mere 0.13% increase in the 10-year Treasury. For a very typical, high quality investment grade account, that offset a substantial portion of a year of potential yield in just 4 days.

ACM is a registered investment advisory firm with the United States Securities and Exchange Commission (SEC). Registration does not imply a certain level of skill or training. All written content on this site is for information purposes only. Opinions expressed herein are solely those of ACM, unless otherwise specifically cited. Material presented is believed to be from reliable sources and no representations are made by our firm as to another parties’ informational accuracy or completeness. All information or ideas provided should be discussed in detail with an advisor, accountant or legal counsel prior to implementation. All investing involves risk, including the potential for loss of principal. There is no guarantee that any investment plan or strategy will be successful. ©ACM Wealth